China will allow provincial-level governments to raise about 1 trillion yuan ($139 billion) via bond sales to repay the debt of local-government financing vehicles and other off-balance sheet issuers, a small step toward addressing one of the biggest threats to the nation’s economy and financial stability.

The Ministry of Finance has informed relevant authorities about the “refinancing bonds” program, people with knowledge of the matter said, asking not to be identified as they aren’t authorized to discuss the program. The quota has been set for each region, one of the people said, without providing further details on sizing.

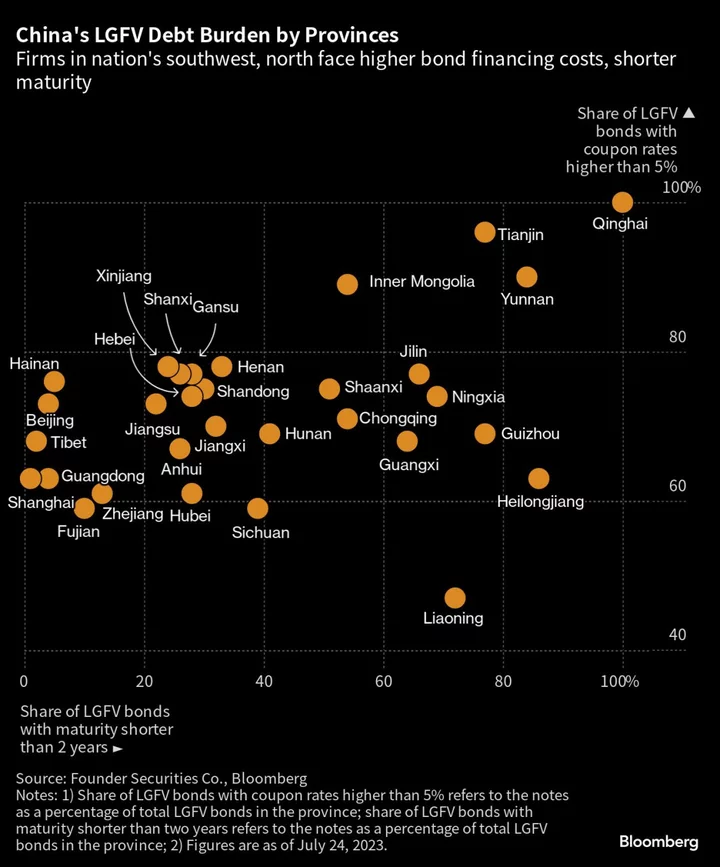

All provincial-level governments but Beijing, Shanghai, Guangdong and Tibet will be able to use the bonds to repay off-balance sheet liabilities, known as “hidden” debt in China, according to one of the people. Authorities also identified 12 provinces and cities as “high-risk” areas where more support will be provided — including the provinces of Guizhou, Hunan, Jilin and Anhui, as well as Tianjin city, one person said.

The program will in effect bail out weaker issuers including LGFVs, shifting the debt burden to provincial governments instead.

The finance ministry didn’t respond to a request for comment from Bloomberg News.

The program comes weeks after the ruling Communist Party’s Politburo, its top decision-making body, said it would use a package of measures to resolve local government debt. President Xi Jinping has previously described the issue as one of the “major economic and financial risks” facing China.

The amount covered under the debt swap program, though, is a drop in the bucket compared to the 66 trillion yuan the International Monetary Fund estimates local government financing vehicles will hold by the end of this year. It’s also far smaller in size than a similar initiative launched by the government in 2015.

Back then, China deployed a massive debt-swap arrangement worth 12.2 trillion yuan for a few years in a bid to lower the amount of off-balance sheet debt carried by local governments. Now widely referred to as “hidden” debt, the term refers to funds raised by government-related entities — such as LGFVs — which borrow from banks and bond markets to finance infrastructure spending and other public projects.

The debt raised is kept off the balance sheets of local authorities, yet is widely considered in financial markets to carry an implicit government guarantee of repayment.

That 2015 program didn’t do much to actually solve the debt issue. The costs of servicing debt have risen in recent years, creating a drag on Chinese fiscal spending. At the same time, many local governments have seen their income drop due to a two-year property market slump and two years of pandemic relief spending. That’s raised the risk that LGFVs will default on their debt, which could destabilize China’s financial system.

Even so, the swap program this time around may help defuse the risks of default faced in the regions where it’s implemented. It can also bring down the financing costs on the hidden debts, give local governments more time to repay, and improve funding conditions in those places. One person said the issuance will be planned in batches.

Unlike a write-off, however, the debt will still have to be serviced — squeezing the room already debt-laden local governments have to sell more bonds to fund infrastructure investment and spur economic growth.

Aside from the scale of the program, there are a few key differences between this debt swap program and the initiative from 2015. The initial debt swap plan involved issuing extra bond quota, while more recent programs including this one are intended to make use of unused quota from prior years. As of the end of 2022, regional governments across the country had a total of 2.59 trillion yuan worth of unused quota, according to Bloomberg calculations based on data from the Ministry of Finance.

It remains unclear how provinces will distribute the quota between different LGFVs under their jurisdiction. Some LGFVs are owned at the provincial level, while others are owned by city or county governments.

Beijing has tried a few other ways to resolve debt woes in recent years. In 2019, some counties in less-developed regions were picked by the government to replace their hidden debt with bonds in a trial program to improve their financing ability.

In late 2020, special local bonds for refinancing purposes were introduced — first as a way for weak regions to reduce their off-balance sheet liabilities, and then as a strategy for rich places including Beijing, Shanghai and Guangdong in southern China to clear hidden debt. Guangdong in 2021 became the first to claim it had successfully eliminated such debt.

While the person familiar with the latest plan didn’t explain why Beijing, Shanghai, Guangdong and Tibet had been excluded from the new debt swap program, those four places either have no “hidden” debt or have very little.