Recession alarms are ringing around Europe’s bond markets, replacing the previous panic over inflation as investors come to terms with the threat to economic growth of increasingly tight monetary policy.

Yield curves from Germany to the UK are now the most inverted in decades as investors pile into long-dated bonds for cover. The euro had its worst week since May and the pound fell on concern the Bank of England risks triggering a contraction. Traders rushed to the safety of the dollar.

A swathe of weak economic data from Germany to France on Friday sealed the shift in focus after the UK’s brutal inflation print and surprise half-point interest rate hike earlier broadcast the threat of stagflation.

Now, attention turns to the European Central Bank’s main conference in Sintra, Portugal. Traders will parse the latest rumblings of top officials from the ECB, Federal Reserve, Bank of England and others for a read on how much more they’re looking to squeeze borrowers. The latest euro-area inflation numbers and German Ifo print will also prove key.

“Data this week has given the recession argument a serious foothold and I’d expect that to continue,” said Gordon Shannon, portfolio manager at Twentyfour Asset Management LLP.

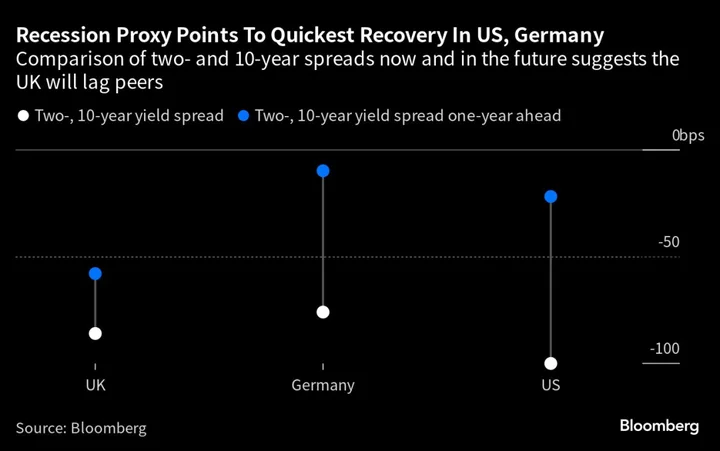

Across the region, bond markets are flashing warnings.

European Yields

Yields are inverted from the norm where investors demand more compensation to hold longer-maturity debt relative to shorter maturities. Instead, near-term rates are higher, implying market expectations for rate hikes followed by cuts as the economy stalls.

German two-year bonds are yielding over 70 basis points more than comparable 10-year securities, the most since 1992. In the UK, it’s over 80 basis points, the most since 2000.

Longer-maturity euro area bonds have found favor in this environment, registering returns of 3.8% this year, more than eight times those of their shortest peers, according to Bloomberg Indexes.

Twentyfour’s Shannon has been positioning for a recession for months, gravitating toward high-quality credit, while holding some exposure to longer-dated UK government bonds.

“Gilt yields are already elevated, and have more potential to rally on recession fear relative to Bunds or to US Treasuries,” Shannon said.

The risk of recession may spur demand for UK bonds, but the prospect of negative growth could spell trouble for the pound.

Sterling has been the best-performer among its G-10 peers so far this year on the view that higher rates would burnish the appeal of UK assets. This week’s dire inflation print and the BOE hike, however, could prompt investors to look beyond the potential high returns and focus instead on economic fundamentals.

“I would expect risky asset markets to start putting more weight on the negative growth implications of tighter monetary policy,” said Guillermo Felices, investment strategist at PGIM Limited.

“That means downward pressure on GBP, despite higher interest rates,” he said.

Signs of this are already starting to emerge, with options traders turning the most bearish on the pound in nearly five months.

Currency Winners

As the prospect of recession typically increases selling of higher-yielding currencies like the pound, those viewed as a shelter stand to benefit.

The Japanese yen’s low-yield status, which has punished it all year, becomes a “safe-haven” characteristic in times of uncertainty.

Van Luu, global head of currencies at Russell Investments, sees a 55% possibility of a global recession in the next 12 to 18 months.

“The global growth cycle is not picking up, but worsening,” he said. “As a tactical play, we like the yen as a defensive currency in this scenario.”

The dollar, widely considered to be the world’s safest currency, is poised to be the biggest winner. Investors are already buying the greenback, helping the Bloomberg Dollar Spot Index snap a three-week losing streak.

“It’s hard to see how the dollar is not going to be supported here,” said Fredrik Repton, senior portfolio manager for global fixed income and currency at Neuberger Berman.

Repton extended his long position in the dollar against the euro ahead of Friday’s weak European PMI readings, betting that the data would amplify recessionary fears in the euro-zone and the divergent growth outlook across the Atlantic.

“The US dollar is seen as a defensive asset class and it’s also offering an attractive carry pickup,” he said.

This Week

- June inflation numbers from the euro area and Germany will be closely scrutinized for the latest cost-of-living trends

- German Ifo figures will provide insights into the country’s economic health

- Bond sales from the EU, Italy and the Netherlands ar set to total around €15.5 billion ($16.9 billion) next week, according to Citigroup Inc.

- The UK sells £4.25 billion of conventional and inflation-linked debt

- The BOE will sell long-maturity bonds from its quantitative-easing era holdings to conclude this quarter’s operations

--With assistance from James Hirai and Greg Ritchie.