The world’s major central banks are approaching a critical juncture in their fight against inflation, with the route they ultimately choose set to impact the economy for years to come.

Their choice is between trusting that the most aggressive tightening in four decades will be enough to damp price pressures that have only just started to ease, or to keep going to insure against concerns that 2% inflation targets are a thing of the past.

Over the next two weeks, the Federal Reserve, European Central Bank and Bank of England must decide how much further they need to push, with the former potentially closest to peak rates. The Bank of Japan also meets amid ongoing speculation it’s approaching the point where it’ll begin to remove stimulus.

Decisions this past week underscored the ongoing battle to tame prices. The Reserve Bank of Australia surprised investors for a second month with another hike and warned its desire to preserve job gains doesn’t mean it’ll tolerate prolonged price pressures. The Bank of Canada, on pause since January, resumed tightening and said the economy is running too hot to bring inflation back to target.

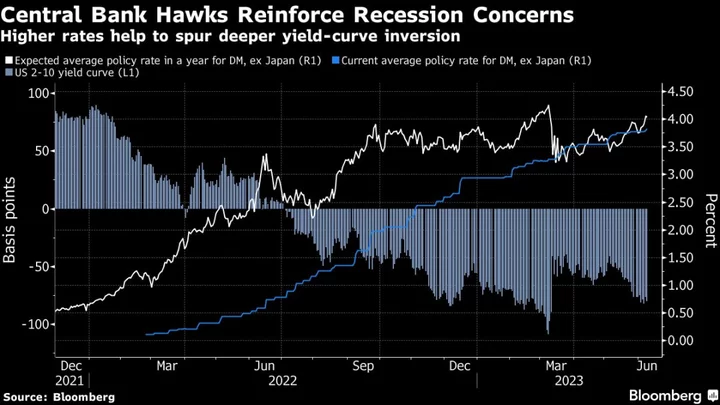

The surprise hikes from Australia and Canada spurred traders to boost expectations for further monetary tightening. Bond investors are responding to that shift by anticipating a greater chance that central banks push their economies toward recession. Yield curve inversions deepened, with yield curves flattening across the US, Germany, UK and Canada.

Complicating central banks’ assessment is the fact that the pass-through of interest-rate increases is playing out differently this time around. Labor markets remain strong as businesses cling to workers amid fears they may not be able to rehire them when needed. And pent-up pandemic savings continue to underpin consumer demand.

None of the choices policymakers have is risk-free.

Pausing or halting hikes and relying on the transmission process may be the safest path to the soft landing everyone wants to achieve. But it also threatens a repeat of the stop-go policies that badly scarred the US in the 1970s if it turns out that more tightening is needed later on.

Moreover, such an approach can entrench inflation expectations, boost wage growth and the housing market — all of which is vexing the RBA’s Philip Lowe right now.

The alternative — continued tightening — is the surer path to defeating inflation, but may wreak havoc on the economy along the way and push the global financial system into a tailspin.

On top of the decisions themselves is the communication challenge: Any pause risks re-igniting animal spirits and fueling already-bullish equity markets, as would a hike that’s accompanied by any hint that this is the end of the tightening road.

Federal Reserve

Going into the Fed meeting on June 13-14, central bank leadership has signaled that it prefers to take a break from a credit-tightening campaign that’s seen interest rates rise five percentage points over the last 14 months.

One big uncertainty that Chair Jerome Powell and his colleagues are monitoring: How much will banks pull back on their loans to companies and consumers in the wake of the recent failure of several regional lenders.

But with inflation proving sticky, policymakers have also been at pains to stress that they’re far from declaring mission accomplished in their drive to bring price pressures to heel.

“A decision to hold our policy rate constant at a coming meeting should not be interpreted to mean that we have reached the peak rate for this cycle,” Fed Governor Philip Jefferson, who’s been nominated to be vice chair, said in May 31 speech in Washington.

European Central Bank

In the euro zone, a quarter-point hike is all but guaranteed when the ECB announces its decision one day later on June 15, with attention focused on policymakers’ public debate over when and where rates will peak.

A bigger-than-expected slowdown in inflation last month and retreating expectations, along with more restrictive credit conditions, will likely embolden those preferring to stop tightening in July — exactly one year after liftoff. That would leave the deposit rate at 3.75%.

But another rate increase in September isn’t entirely off the table, not least as far as some of the Governing Council’s more hawkish members are concerned.

President Christine Lagarde herself told European lawmakers this week that price pressures remain too strong.

“Although some are showing signs of moderation, there is no clear evidence that underlying inflation has peaked,” she said.

Bank of England

The policy dilemma is perhaps most stark for the Bank of England. On the one hand, inflation is higher, at 8.7%, and tightness in the labor market makes a dreaded wage-price spiral an ever-present threat. On the other, the International Monetary Fund forecasts the UK to grow just 0.4% this year.

Interest rates are already squeezing the economy at 4.5% and markets expect them to top 5%. A quarter point hike is nailed on for June 22.

Howard Davies, chair of NatWest Group and former BOE deputy governor, says policy takes about 18 months to feed through. “We are now entering the period where tightening starts to be felt.”

For the moment, though, the overriding concern is credibility. Politicians have attacked the BOE for missing the inflation threat and a second failure would be considered almost unforgivable.

Bank of Japan

With inflation above its 2% target for more than a year now, the BOJ may be finally getting closer to inching away from its emergency policy settings, according to some economists.

No major shift is anticipated when officials meet on June 16, though economists including those at Goldman Sachs and BNP Paribas expect the BOJ to tighten policy next month — even as Governor Kazuo Ueda has insisted that he sees no immediate need to change course.

He argues that — after years of deflation — the cost of making premature policy adjustments is larger than that of waiting. Workers’ real wages are still declining, weighing on consumer spending power so urgently needed to sustain inflation at 2%.

Still, any movement away from the BOJ’s ultra easy policies will be less disruptive if they happen when other big global central banks are still tightening, meaning the door may close on Ueda if he waits too long.

--With assistance from Toru Fujioka and Garfield Reynolds.

Author: Jana Randow, Rich Miller and Philip Aldrick