Stock markets that have refused to buckle under the highest yields since 2007 face a new test. Third-quarter results will shine a light on how much those rates are already hitting profits — and what they’ll do to lofty equity valuations.

As the earnings season kicks off, corporate managers will likely be peppered with questions about how long balance sheets can resist pressure from high interest rates. The longer rates stay high, the more onerous debt refinancings will get. New projects could also be reviewed, lowering corporate investments in growth.

Some $820 billion of US and European non-financial corporate bonds are maturing in the next 12 months. That’s about 7% of this market, according to data compiled by Bloomberg. While companies overall are not expected to run up against a maturity wall before 2025 onwards, debt-ridden companies are already feeling the pain from higher rates.

“The sword of Damocles has been hanging over highly indebted companies for a number of quarters,” said Patrick Armstrong, chief investment officer at Plurimi Wealth. “3Q earnings may see this sword drop.”

Goldman Sachs Group Inc. strategists led by David Kostin recently warned that borrowing costs for S&P 500 companies have already ticked up by the largest amount in nearly two decades, on a year-on-year basis. Of the 69 basis points of contraction in ROE in the first half of the year, nearly half came from higher interest expenses, they said.

Since the global financial crisis, falling interest costs and greater leverage have accounted for nearly one-fifth of an overall 8.8 percentage points increase in the return on equity (ROE) of S&P 500 firms. The risk of rates now being higher for longer could prevent firms from taking on more leverage, hitting long-term profitability, the strategists added.

Read: El-Erian Warns of ‘Massive’ Corporate Refinancing Next Year

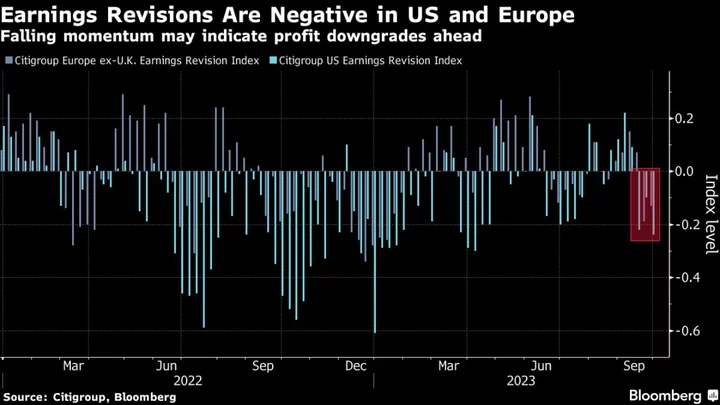

Still, Kostin’s base case scenario is that margins will trough this year, while moderate expansion will follow in 2024 and 2025. “We forecast margins for the aggregate S&P 500 index and most sectors will remain near their 10-year highs,” Kostin wrote in a note on Friday. “While easing input cost pressures and operating leverage should support margins, significant margin expansion appears unlikely due to resilient wage growth as well as higher interest rates and taxes.”

For Marija Veitmane, senior multi-asset strategist at State Street Global Markets, large caps with strong balance sheet stocks are safer bets, over industries tied to the business cycle and economic growth. “We expect the economy to slow down substantially next year, so we’re likely to see very conservative guidance from the managements.”

Megacaps aren’t safe from rate risk either. Growth shares like Nvidia Inc. and other tech darlings derive much of their high values from expectations of future profits. When these are discounted at higher rates they look less attractive.

Nasdaq 100 equities trade at 23 times forward earnings, 25% above the S&P 500 — whose own valuation is inflated by the same tech megacaps. Versus sales, the Nasdaq fetches a multiple of nearly four, almost twice as expensive as the broader market.

“More than 70% of S&P 500 valuations are driven by the long-term growth outlook, hence US equities are extremely sensitive to bond yield moves,” wrote Societe Generale SA strategists led by Manish Kabra in a note last week.

Meanwhile, the equity risk premium, a measure of the differential between stocks and bonds’ expected returns, is getting squeezed, drawing investors out of stocks.

“In a higher rates regime, valuations matter more,” said Barclays Plc strategist Emmanuel Cau, adding that misses are “likely to be punished” due to lofty expectations for 2024 earnings.

LVMH shares slipped in the US after the luxury giant’s sales growth softened in the third quarter as shoppers reined in spending on high-end Cognac and costly handbags — more evidence the post-pandemic luxury boom is waning.

--With assistance from Sagarika Jaisinghani, Tasos Vossos and Allegra Catelli.

(Adds LVMH results in last paragraph)