The Federal Reserve’s policy statement is setting up to be the No. 2 event on Wednesday, with investor focus instead likely to be on the Treasury Department’s new borrowing plan, due hours ahead of the interest-rate decision.

The so-called quarterly refunding announcement will reveal the extent to which the Treasury will ramp up sales of longer-term debt to fund a widening budget deficit. Those securities have been tumbling for weeks, even amid signals from Fed officials they’re “at or near” the end of rate hikes.

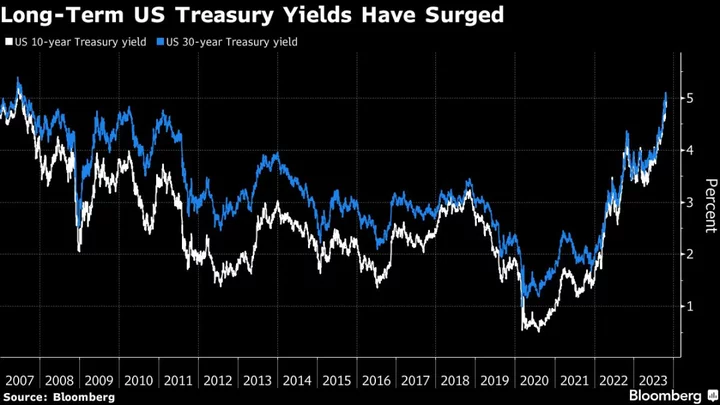

The selloff has sent yields to the highest levels since before the global financial crisis — making longer-term Treasuries more costly for the government. Investors are eager to see whether officials maintain the pace of increase in longer-term debt sales they announced in the August plan. Bumpy auctions of some securities in recent weeks have only increased that focus.

“Market participants are really hyper-focused on supply now and we kind of know the Fed is on hold,” Angelo Manolatos, a strategist at Wells Fargo Securities, said in a telephone interview. “So the refunding is a bigger event than the FOMC. It also has a lot to do with the moves we’ve seen in yields since the August refunding.”

Many bond dealers predict a refunding size of $114 billion, representing the same cadence of increases per each refunding security as laid out in the $103 billion August plan, which marked the first step up in issuance in more than two years.

An alternative view predicted by several large dealer firms would be a smaller bump in longer-term debt, given the surge in yields, and greater reliance on bills, which mature in a year or less. Some see this tweak potentially combined with a signal that a further increase of long-term sales isn’t certain for the next refunding, in February.

“Looking at the refunding, the composition of Treasury issuance might be very consequential and relevant” to the market, said Subadra Rajappa, head of US interest rates strategy at Societe Generale SA. As for the other Wednesday event, “this meeting is sort of a placeholder for the Fed,” she said.

Indeed, Fed Chair Jerome Powell — a former Treasury official himself — and his colleagues may take interest in investor reactions to the refunding. He and others, including Dallas Fed President Lorie Logan, who previously oversaw the Fed’s market operations, have said the surge in long-term yields may mean less need to raise the benchmark rate.

Yellen’s Rebuff

Ten-year yields were around 4.8% at the end of last week, well over three quarters of a percentage point higher than before the August refunding. Yields remained high even after the outbreak of the Israel-Hamas war three weeks ago – the kind of geopolitical flashpoint that can spur haven demand for Treasuries. Israel’s weekend invasion of Gaza will again test previous norms.

While Treasury Secretary Janet Yellen on Thursday rejected the idea yields were climbing due to swelling federal debt, Powell this month did list a focus on deficits as a potential contributing factor.

Read more: How Rising Rates, US Debt Brought Back Term Premiums: QuickTake

Earlier this month, Treasury data showed the federal deficit roughly doubled in the fiscal year through September compared with the year before, effectively reaching $2.02 trillion. The worsening trajectory helped prompt Fitch Ratings to strip the US of its top-tier AAA sovereign rating on the eve of the August refunding.

On Monday, the Treasury will set the stage for its issuance plans with an update of quarterly borrowing estimates, and for its cash balance. In August, officials penciled in net borrowing of $852 billion for October through December. Lou Crandall at Wrightson ICAP LLC says he’s not expecting any downward revision in Monday’s update.

US debt managers in August lifted the refunding issues, which include 3- and 10- and 30-year Treasuries, by $2 billion, $3 billion and $2 billion relative to each of those securities’ previous auctions of new debt. They also increased issuance of all other note and bond maturities, something dealers see happening again this time.

A $114 billion plan for Wednesday would mean the following upcoming quarterly refunding auction sizes:

- $48 billion of 3-year notes on Nov. 7

- $41 billion of 10-year notes on Nov. 8

- $25 billion of 30-year bonds on Nov. 9

The JPMorgan Chase & Co. rates team is looking for a “rinse, repeat” of August. That, they say, was also signaled by Josh Frost, the Treasury’s assistant secretary for financial markets, in a talk last month.

That’s not the universal view, however. Wells Fargo, Goldman Sachs Group Inc., Barclays Plc and Morgan Stanley are among those expecting the Treasury to tilt this time more toward short-term securities, in part given the rise in long-term rates.

Read more: Barclays Predicts Treasury Is About to Slow Terming-Out of Debt

Solid demand for Treasury bills, which yield well over 5%, means there would be ready buyers, but bills currently make up more than 20% of marketable Treasuries. That’s slightly above the recommended range of 15% to 20% laid out by the Treasury Borrowing Advisory Committee — a panel including dealers and investors. Even so, in August, TBAC said it’s comfortable with bills temporarily taking a larger share.

While the government has a longstanding pledge to be “regular and predictable” with its debt-issuance plans, the group of dealers forecasting a change in the pace of the expansion in note and bond auctions argues that the Treasury’s credibility would remain intact. That’s in the context of the August TBAC guidance on bills and an expected lift in auctions of all coupon-bearing maturities.

Besides issuance plans, investors will also be looking for an update from the Treasury of its progress in assembling a program of buybacks of existing securities. The department has said those will start in 2024.

The deficit isn’t the only dynamic forcing the government to borrow more from the public. The Fed is running off its holdings of Treasuries at a pace of up to $60 billion a month. Powell cited this process, known as quantitative tightening, as another potential contributor to the rise in long-term yields.

Next February

It all means the department may have little option over time.

“Treasury will have to again raise funds across the maturity spectrum” on Nov. 1 and again in February, said Praveen Korapaty, chief interest-rate strategist at Goldman Sachs. Goldman’s economists don’t see Fed QT ending completely until early 2025.

The backdrop is ripe for volatility after the 8:30 a.m. refunding details hit the wire.

“Treasury does make adjustments based on how markets are receiving supply,” Korapaty said. “Right now the market is telling you that if you are putting more duration supply in then the market clearing price is going to be higher.”

--With assistance from Elizabeth Stanton and Carter Johnson.