A rally in Turkey’s hard-currency bonds may falter without a more ambitious government tilt toward orthodox monetary policies, investors warn.

The country’s dollar sovereign bonds have returned 8.4% since the first round of voting on May 14, more than twice the average rate of those in other emerging markets, according to data compiled by Bloomberg. Meanwhile, Turkey’s credit-default swaps have tightened more than 300 basis points since the elections to below 400 basis points, the lowest since September 2021.

Investors had hoped a fresh approach by the central bank following President Recep Tayyip Erdogan’s election victory in May would lead to sharply higher interest rates and less use of reserves to prop up the lira. Instead, they say that progress has been disappointing.

Paul Greer, portfolio manager at Fidelity International, says he’s “underwhelmed” by the policy changes so far.

“Given Turkey’s large external financing requirement, large current-account deficit and inadequate monetary policy, we expect the rally to slow down from here into August,” he said. Greer is underweight Turkish sovereign bonds and expects spreads to widen from current levels.

Erdogan, a long-time advocate of lower rates, pledged to install a finance team with “international credibility” following the May vote. He named market veteran Mehmet Simsek as finance minister, and picked Hafize Gaye Erkan, who had previously worked in the US at Goldman Sachs Group Inc. and was a former co-chief executive officer of First Republic Bank, as central bank governor.

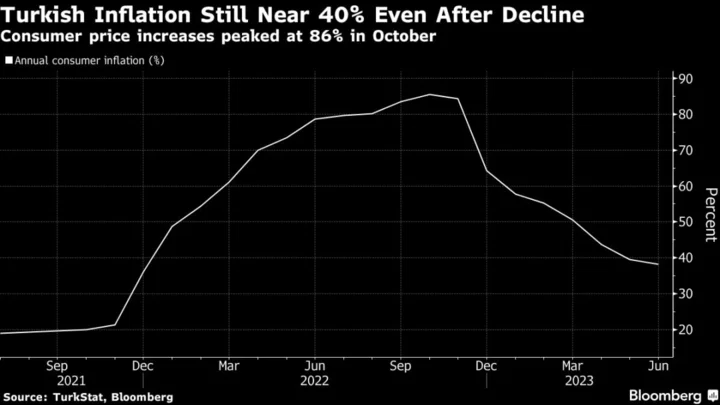

On Thursday, Erkan warned that inflation was poised to jump to 58% by the end of this year, and a peak of 60% next year, from 38% in June, but also said that a “gradual and stable” tightening cycle would continue. This raised questions about how mild interest-rate hikes could rein in anticipated price gains. Inflation rose as high as 86% last October.

Orthodox Policy

“For spreads to tighten materially from here, we need to see sustained implementation of orthodox monetary policy,” Gordon Bowers, a London-based analyst at Columbia Threadneedle Investments, said.

Investors have already been disappointed with the restrained rate hikes since Erkan took the helm, a cumulative rise of just 9 percentage points over two meetings. The central bank began in June to raise its benchmark interest rate for the first time in more than two years, but the increase to 17.5% still leaves real rates way below zero when adjusted for price gains.

Not everyone agrees. The quality of the new economy team, the fact that rate policy has changed direction, and government deals with Gulf countries, all point to sustained investor interest, according to Tim Ash, an emerging markets strategist at RBC Bluebay Asset Management.

Erdogan has long opposed high interest rates, arguing contrary to mainstream thinking, that higher rates will cause faster inflation. Three previous governors who didn’t toe the line ended up being removed by the president. Erkan on Thursday said the central bank was “fully independent” when asked about Erdogan’s influence in monetary policymaking.

On Friday, Erdogan made a further move to revamp his economic team, installing three new central bankers as deputies to Erkan, including a former adviser at the Federal Reserve Bank of New York.

Inflation is only one reason why investors think the rally in debt market will be short-lived. Politics, a record current-account deficit and lira volatility are other key areas of concern.

Todd Schubert, senior fixed income strategist at Bank of Singapore, said that a sustained rally would require “a more forceful policy of structural reforms and monetary policies from Simsek and Erkan.”

(Updates with comment in 10th paragraph.)