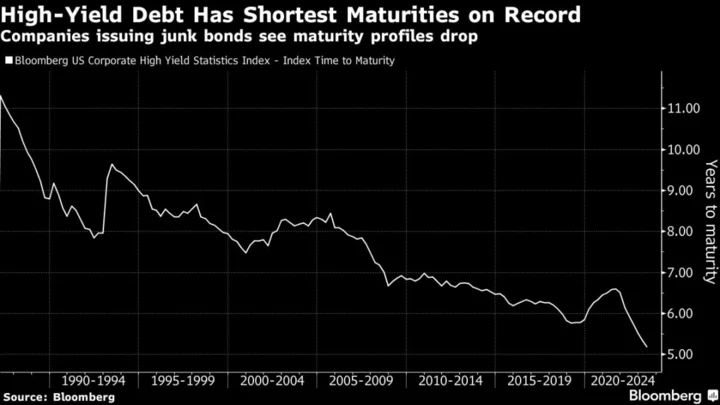

US junk bonds have the shortest average time to maturity on record, signaling that companies will have large amounts of debt to refinance in the next few years.

The average time to maturity for high-yield debt has fallen to just 5.18 years — the shortest it’s been since Bloomberg started tracking its high-yield corporate index in 1987. In comparison, the average maturity on an investment-grade bond is 11 years, Bloomberg-compiled data shows.

“Shorter maturity is helping lead to shorter duration that theoretically creates less volatility, but it also is likely leading to shorter maturity walls,” writes Bob Kricheff, portfolio manager and global strategist at hedge fund Shenkman Capital. This can cause problems, especially if financial liquidity tightens too much, he noted.

“As long as capital markets stay liquid and we continue to see issuance, it shouldn’t be a problem,” Kricheff said in an interview. “If not, companies will have trouble reaching maturities.”

Frozen capital markets led to corporate defaults during the global financial crisis of 2008, Kricheff pointed out. That crisis was sparked by the meltdown in commercial mortgage-backed securities. In 2011, both equity and credit markets froze again for about six months, after the US came close to breaching the debt ceiling and was slapped with a credit rating downgrade. In March 2020, liquidity evaporated on Coronavirus fears and lockdown measures.

Cause and Effect

A slowdown in overall issuance in the high-yield primary market as well as increased demand from investors for shorter-term paper are both largely responsible for bringing maturity dates forward, according to Kricheff.

Riskier borrowers opted out of the primary market as interest rates soared, looking instead to floating-rate leveraged loans and private credit-sponsored financings. That’s pushed down the amount of US junk bonds issued by about 13%, to $1.38 trillion, from an October 2021 peak, data compiled by Bloomberg shows. The record issuance that year also built up a large refinancing pipeline.

“It does feel right now there’s a good pace of refinancing,” Kricheff said. “It’s a question of whether it can continue and push off maturity walls.”

Junk bond issuance in May amounted to $22.6 billion, of which 70% went toward refinancings and 24% for funding mergers and acquisitions, wrote Bloomberg Intelligence credit strategist Noel Hebert earlier this month.

Meanwhile, the supply of shorter-dated junk notes has climbed, as jittery investors ask for accelerated due dates on concerns that corporate defaults will rise as a possible recession draws near.

“The two trends have combined in force causing a dramatic move in average maturity,” Kricheff noted. “This move has been much more dramatic than the shift in OAD (that IMO gets more focus).”

Another reason for the shrinking maturities is the exodus of Covid-era fallen angels that have recovered, according to Andrzej Skiba, Head of BlueBay U.S. Fixed Income at RBC Global Asset Management. Those borrowers expanded overall maturities on being downgraded, which contracted again as they ascended.

For example, Occidental Petroleum Corp., The Kraft Heinz Co. and Western Midstream Partners were longer duration issuers that spent a brief stay in the junk market before regaining their investment grades.

Demand for Deals

Companies across the speculative-grade spectrum are finding demand for five-year paper. Short-duration mutual funds and strategic income funds are among the buyers of the notes, according to Skiba.

“In the past, this was more of a domain of CCC issuers or those with really challenged business models or lack of sponsors,” he said. “Out of the combinations of maturity and size that was acceptable to the market, shorter maturity was more appealing to investors.”

Sealed Air Corp. in January wrapped a $775 million, five-year deal to help finance its acquisition of LB Holdco, the parent company of Richmond, Virginia-based Liqui-Box. The packaging manufacturer’s offering carried a BB+ rating with a coupon of 6.125%. In March, Canadian auctioneer Ritchie Bros Auctioneers Inc. sold $550 million of BB+ rated bonds, also due 2028 and carrying a 6.75% coupon, to help fund its takeover of IAA Inc.

Last week, real estate investment trust Ryman Hospitality priced $400 million of B tier five-year notes with a 7.25% coupon to support its purchase of a Texas resort and spa.

--With assistance from Olivia Raimonde.