Japan’s era of negative interest rates will end in coming months, and the implications for world markets will be enormous, with US Treasuries set to suffer the most, according to the latest Bloomberg Markets Live Pulse survey.

The Bank of Japan is likely to unwind its unusual policy of sub-zero rates during the first half of 2024, the majority of 315 respondents said. The move would bring an end to a bold experiment it embarked on in 2016 — one that’s recently placed Japan at odds with other major central banks that have been tightening aggressively to combat inflation.

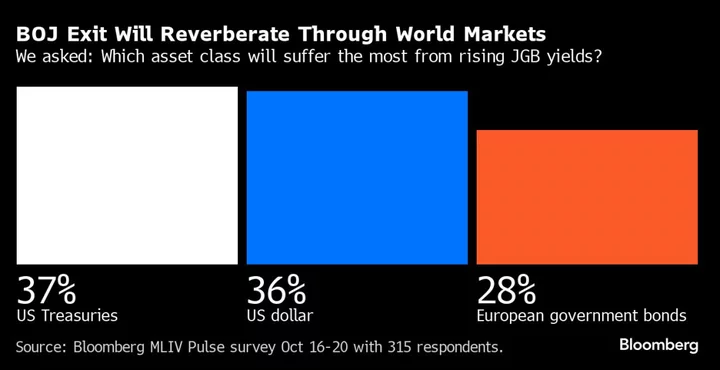

What the BOJ does, and when it does it, will reverberate through world markets. The biggest consequence, according to MLIV Pulse respondents: more turbulence for the vast amount of Treasuries. That’s because higher yields in Japan would encourage fund repatriation by Japanese investors whose huge holdings include US, European and Australian debt.

“A shift in the BOJ’s policy could slow the export of capital from Japan as yields become more attractive locally than they were before,” said Martin Whetton, head of financial markets strategy at Westpac Banking Corp. in Sydney.

Thirty-seven percent of participants said Treasuries will face the most severe impact from Governor Kazuo Ueda shifting away from super-accommodative policy. Declines in the dollar may add to the misery, as 36% expect pain for the currency that the US debt is denominated in.

Portfolio managers and central banks around the world are keeping a watchful eye on any move by the BOJ, which has made negative rates and yield curve control the cornerstone of its policy to fight stagnant prices. It rocked global markets by raising the cap on benchmark 10-year bond yields in late 2022, and again at the end of July, pushing up bond yields.

“Some form of normalization is probably necessary,” said Eugene Leow, a senior rates strategist at DBS Bank Ltd. “This could mean upward pressure on five- to 10-year developed-market yields as higher Japanese government bond yields spill over.”

Japanese investors are the biggest foreign holders of US government bonds, with more than $1.1 trillion at the end of August, according to data from the US Treasury Department. Life insurers dumped a net ¥196 billion ($1.3 billion) of foreign bonds in the April-September period, following a record ¥8 trillion of sales in the previous six months, according to Ministry of Finance data.

The MLIV Pulse survey shows that 61% of respondents expect global bond market volatility to increase when the BOJ changes the policy, with majority of respondents predicting the historic step will happen next year.

“The market will probably be very jittery until traders and investors will get used to a world with positive yields,” said Ayako Sera, a market strategist in Tokyo at Sumitomo Mitsui Trust Bank Ltd. “It’s like a big stone being thrown into a pond where there has been no wind.”

Treasuries, traditionally the pillar of stability in many saving and investment portfolios, are already more volatile than stocks, at least by one measure. The combination of the aggressive policy tightening by the Federal Reserve and the flood of bond sales by the US government have imposed historical losses, especially on long-duration debt.

The survey asked participants when they thought benchmark Japanese 10-year sovereign yields would reach 1%, the effective limit tolerated by the BOJ. That level is likely to be touched in the first half of 2024, according to 43%, or even later, per 16% of respondents.

Japan’s 10-year yields have almost doubled since late July, when the BOJ increased the cap. At 0.835%, though, they’re still far below 4.91% for their US counterparts.

This yield gap has been widening, making the yen into worst performer among Group of 10 currencies so far this year. The Japanese currency has lost more than 12% against the greenback this year, ending last week at 149.86 per dollar.

The vast majority of survey respondents, at 62%, predict the dollar-yen rate to finish the year in a range of 140 to 150.

The MLIV Pulse survey of Bloomberg News readers on the terminal and online is conducted weekly by Bloomberg’s Markets Live team, which also runs the MLIV blog. This week, are asking which is a better investment, the Ozempic maker Novo Nordisk or the AI chip leader Nvidia. Share your views here.