Volatility is rising in UK bond markets ahead of a knife-edge interest-rate decision from the Bank of England.

While money market pricing and economist surveys tilt toward a quarter-point hike on Thursday, investors are bracing for a surprise, with Goldman Sachs Group Inc, HSBC Holdings Plc, Barclays Plc and UBS Group AG envisaging 50 basis points of tightening.

The contrast with the well-telegraphed, quarter-point hikes delivered last week by the Federal Reserve and the European Central Bank couldn’t be starker. More than a year-and-a-half into the BOE’s hiking campaign, the market is still in the dark over how much tightening it stands to deliver to combat inflation.

And it speaks to the challenges officials face in balancing the need for tighter policy against moves that could hobble growth.

There is a “high degree of uncertainty on the Bank’s reaction function given the dearth of Monetary Policy Communication,” said a Barclays team including Mariano Cena. “Data and developments since the June meeting do not point squarely to either a 25 basis-point or 50 basis-point hike.”

Gauges of rates volatility in the UK have been increasing — even as their dollar and euro equivalents fall back. The pound is up over 6% this year, buoyed by BOE rate-hike expectations, creating a high bar for further gains should the central bank not deliver.

UK Bond Rally on Inflation Miss Through Lens of Options Market

As some investors bet on an end to hikes from the ECB and Fed, the BOE runs the risk of becoming what BNP Paribas calls the “last hawk standing” — diminishing the appeal of holding UK bonds. Last year’s rout in gilts, during Liz Truss’s chaotic premiership, proved that even one of the largest bond markets in the world is vulnerable to sudden idiosyncratic risk.

No Easy Choice

Should the central bank deliver a quarter-point cut, Ales Koutny, head of international rates at Vanguard, says he’d reconsider an assumption the BOE was getting tough on inflation, and possibly reduce his long position in 10-year gilts.

“If they go down to 25 basis points this meeting, just because we had one somewhat more benign inflation print, and then we get some stronger data next month and they’re back to 50 basis points, markets are going to start putting a lot of premium in terms of the uncertainty,” he said.

Citi strategist Jamie Searle, meanwhile, says a half-point hike would be more problematic.

“Delivering 50 basis points would, in our minds at least, make the MPC’s reaction function more confusing,” Searle said. “The risk of overkill also grows later in the cycle. Our ongoing concern is that this may be a ‘Wile E. Coyote moment’ for the UK economy.”

A quarter-point hike would result in money markets pricing a peak BOE key rate of 5.75%, according to Searle. A 50 basis point increase could see it rise back to between 6.25% to 6.50%. Current market pricing implies a peak slightly above 5.85%.

In recent months, Bailey has watered down guidance pointing toward sharp rate hikes, making further action conditional on more evidence inflation will persist. That led to an acceleration in the pace of rate hikes in June, when the BOE delivered an unexpected half-point increase.

BNP analysts point to the nine-member Monetary Policy Committee’s last decision, which said it “had become more important” to weigh developments in the rental market. Since then, inflation data has pointed to “runaway rents” while pay data is “way too hot,” they said.

“The BOE only has a couple of opportunities to tighten rates without becoming the last hawk standing,” wrote Matthew Swannell and Paul Hollingsworth, who expect a half-point hike. “Now is not the time to stop.”

Mixed Data

When it meets on Thursday, the Monetary Policy Committee must balance a raft of mixed data.

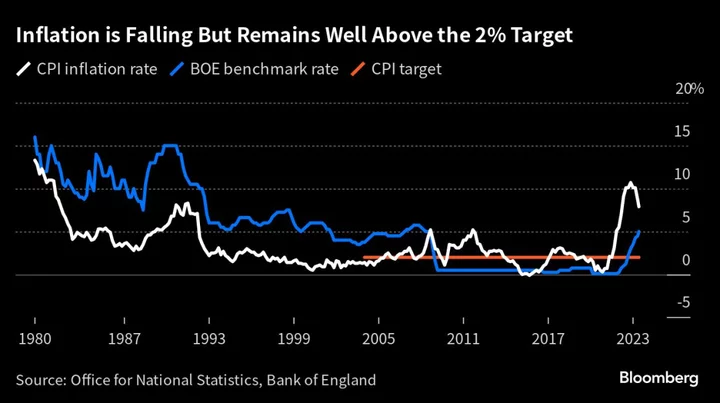

On the one hand, the latest reading showed inflation fell below 8% for the first time in 15 months in June. While other gauges are also in retreat, they remain much higher than the BOE’s 2% target.

So far, the economy seems to be responding slowly to the swift surge in rates. Economic growth has held up better than expected, and retail sales have been surprisingly strong for much of this year, with worker shortages driving up wages and putting more money in consumers’ pockets.

While Prime Minister Rishi Sunak has voiced support for the BOE, arguing that containing inflation is one of his five top priorities, he’s also eager to get growth on track before an election expected next year.

Traders are all too aware of the BOE’s record for surprises.

At the start of the tightening cycle, markets were caught out by officials voting not to hoist the key rate from 0.1% to 0.25% in November 2021. A month later, the BOE did hike, but this time investors were braced for no change due to the return of coronavirus restrictions.

And the scope of the hikes adds another element of surprise. The BOE has accelerated from as little as 15 basis points all the way to 75 basis points.

“The UK bond market is on a wild ride with no guidance from the BOE between meetings and large inflation data surprises having become the norm,” said Tanvir Sandhu, chief global derivatives strategist at Bloomberg Intelligence. “The greater uncertainty around the terminal rate compared to the US and Europe may make it the last to see volatility normalize.”

--With assistance from Naomi Tajitsu, James Hirai, Reed Landberg, Harumi Ichikura and Andrew Atkinson.